It is possible that investors will remember the summer of 2024 as the turning point, the beginning of the end, the moment things started to unravel. But take away the emotional jolt that always accompanies a reversal in sentiment and the evidence suggests otherwise.

It is highly plausible that stocks go back to climbing the proverbial ‘wall of worry’ and that August 2024 is quickly forgotten.

What next?

I expect a broader range of sectors will start contributing to the rise of equity markets. Up until now, a narrow sub-set of the 1,429 MSCI World Index constituents have done the heavy lifting in driving the bull market.

Most of them are large companies that have been better positioned than smaller businesses to weather higher interest rates. A few mega-cap tech stocks have led the way, their earnings and earnings expectations boosted by the boom in demand for artificial intelligence (AI).

But while companies associated with this theme may still have room to run, investor interest has come with growing scrutiny over elevated valuations and the pace at which these businesses are managing to monetise AI.

Interest rate expectations are also beginning to shift. Fresh momentum for the broader market will therefore need to come from companies that have been out of the limelight, where earnings expectations – and multiples – are much lower.

Catch-up trades

Don’t be surprised if that’s what happens. Encouragingly, small- and mid-cap stocks that were left behind have started to catch up with market leaders in the US and the UK as they are set to benefit from falling interest rates.

There are also mid-cap stocks caught up in the sell-off – in software, for example – that have strong business models and now trade attractively. It’s a good set-up for early cyclical sectors as well as for prioritising value over growth.

In Japan, the August correction has helped close the gap between smaller companies and the rest of the market. Japanese equities have a lot to offer at only a 15x price-to-earnings (P/E) ratio (the S&P 500 was trading at 24x at the time of writing).

Near-term volatility shouldn’t stifle the country’s multi-year corporate governance reforms, which are prompting companies to eliminate idle assets and cross shareholdings.

In fact, through our own company engagements, we know the movement to drive shareholder returns has broadened out to mid-caps.

The catch-up trade applies to countries, too. There’s value to be found in the UK, for example, where the market is trading at around 12x P/E, topped up with a 4% dividend yield.

The UK may have made headlines recently for the wrong reasons but that doesn’t change the fact that policy is supportive. The Bank of England has begun to cut interest rates and the market is relaxed about the new government, helped by its emphasis on economic growth, political stability, and housebuilding.

In other words, attractive entry points are now available to investors in many regions and in styles that enjoy a range of favourable conditions, where multiple compression is much less of a concern compared to the more crowded corners of the market.

After the dust settles

Times like these are made for investors who focus on fundamentals. When sentiment is fickle, things can turn quickly, even when fundamentals are sound. A few economic data points and policy statements can spark immense volatility and contagion, just as we saw recently in the US and Japan.

Yet for all the talk of a US recession, consumers’ and companies’ balance sheets remain resilient. A soft landing is still the most probable outcome. And the sell-off did nothing to change the trajectory in Japan, where reflation is emboldening companies to expand margins, increase capital expenditure, and return more cash to shareholders. Equities have already regained some ground, with smart money snapping up bargains.

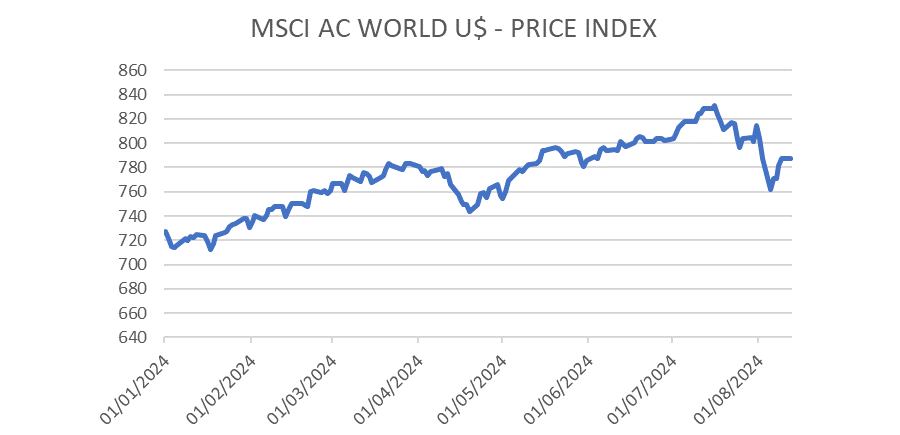

And from the perspective of a global equity investor, stocks remained in positive territory for the year throughout the recent sell-off.

Stocks go up, though not in a straight line

Source: Fidelity International, Refinitiv Eikon Datastream, MSCI All Country World Index, August 2024.

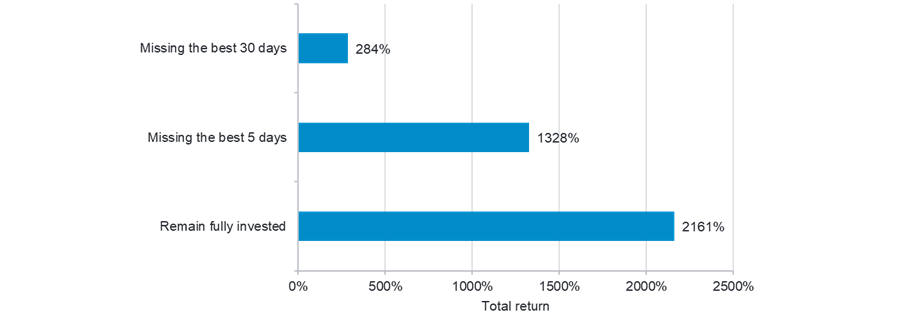

Staying invested is usually much smarter than being scared out of positions by volatility. The benefits of equity investing come from its long-term compounding effect, which is undone by short-sighted reactions.

Anyone who stayed invested since 1993 in the S&P 500 would have generated returns of over 2,100% up to the week ended 2 August 2024. But had they missed the five best days of that period, that would fall to just 1,328%. It dwindles to 280% if we take out the best 30 days.

The price of fear

Source: Fidelity International, Refinitiv Eikon Datastream, August 2024.

And you can tell a similar story for every equity market around the world. If there’s one thing I’ve learnt from decades in asset management, it’s that stock markets don’t go up in a straight line. Staying invested in a diversified portfolio is almost always the smartest strategy.

Niamh Brodie-Machura is co-chief investment officer of equities at Fidelity International. The views expressed above should not be taken as investment advice.