It has been hard to consistently produce top returns over many different timeframes, particularly in recent years, with the Covid pandemic, rampant inflation and rising interest rates benefiting different types of stocks at different times.

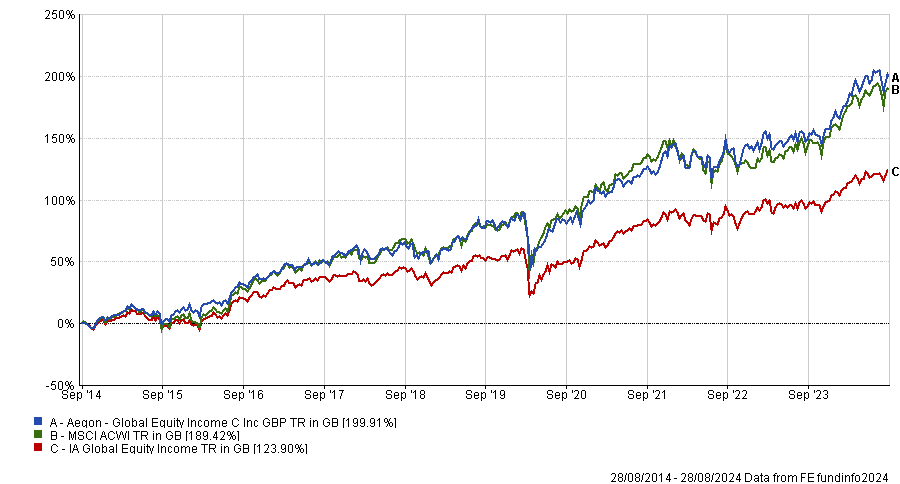

Yet Aegon Global Equity Income has managed to achieve a top-quartile return in the IA Global Equity Income sector over one, three, five and 10 years. There are many reasons for this, including the fund’s large technology weighting.

Below, co-manager Mark Peden talks more about how he “hates” the value end of the market and why many income funds are “rather disingenuous”.

Performance of fund vs sector and benchmark over 10yrs

Source: FE Analytics

What is your process?

We are quality income managers who buy between 40 and 50 stocks, which all display the same characteristics: a premium dividend yield to the market; a growing dividend over time; a strong balance sheet; a well-covered dividend; and a decent return on equity. If a company passes on four of those filters then it is of interest to us.

We do not require all of them because we want to own some lower-yielding companies in our fund. But our income sweet spot is a dividend yield between 2% and 4%. That is where the bulk of the portfolio is focused.

We do this because it gives us the best opportunity to deliver on all our targets: a premium income stream that can grow over time above inflation all while delivering attractive total returns.

Why should investors pick your fund?

I find that a lot of the funds in the sector are being rather disingenuous in calling themselves an income fund because they offer distributed income that is in-line with the market.

Our target is to distribute an income stream around 30% higher than the market that can grow over time, which is why we target companies that have a track record of growing the dividend.

Is 2.3% enough of a yield for most investors?

All yield targets are relative. Markets are reasonably elevated and a 1.7% dividend yield [for the MSCI ACWI benchmark] does not compare particularly favourably to a risk-free rate around 3.8%.

However, I think it is unfair to compare an equity yield to a fixed income fund because when you buy fixed income instruments the coupon is fixed whereas with a yielding equity you get growth in the dividend over time.

Aren’t income funds mainly associated with value investing?

A lot of people equate equity income investing to value investing and that is not what we do. In fact, we actually hate the value end of the market.

Value guys target the high-yielding part of the market, which leads them into some structurally challenged areas. By doing that they essentially give up a lot of opportunity for capital return.

If we were targeting telecom, oil, utilities and real estate stocks we could get a yield that is competitive with the risk-free rate but our total return would be absolutely crap.

I don’t think our investors would be happy if we were sacrificing the ability to grow capital and income to be sat in the fourth quartile of our sector but with a yield 150 basis points higher than we currently are.

You have a high weighting to technology stocks. Why?

A quarter of the fund is in tech, which is essentially the same as the market but is a hell of a lot more than the style index. Technology as a sector has provided the best income growth over any time period and, let’s face it, artificial intelligence (AI) has been the only game in town. We wanted our investors to have exposure that.

We are all about large-cap, established, quality tech. Our portfolio is invested in established tech such as Microsoft, Broadcom, Taiwan Semiconductor Manufacturing Co. (TSMC) and Samsung, which are arguably lower-beta companies versus Crowdstrike, for example.

Why Microsoft and not the other big tech names?

Microsoft trades with a larger yield of around 0.8%: bigger than Apple, which is 0.45%, or the new dividend kids on the block. These guys are all trading with a yield of sub 0.5%.

If we owned these stocks, it would have a diluting impact on the overall fund yield and we would have to rely on the rest of the portfolio to do the heavy lifting to deliver the premium income we promise investors.

What has been your best holding recently?

Over the past 12 months our top attributing stock has been Broadcom – a technology conglomerate with big interests in the semiconductor and infrastructure software space.

We’ve been using Broadcom pretty much as our Nvidia hedge. It is quite correlated to Nvidia because it is plugged into the AI fairy dust. It makes a lot of the custom chips for the big data centre players.

Shares are up 80% in the past 12 months. It is the second-largest position in the fund and by mid-July it had got to 8% of the portfolio. We have cut it back, selling about 40% of the position down to around 5%, which was rather well-timed.

And your worst?

In absolute terms it was probably Telecom Indonesia. It has been an absolute bag of spanners, which we have now sold. It is down 20%.

But the worst attributer is Nestlé, which is a classic income stock. Consumer staples should have bulletproof operations and balance sheets but it has come off the ball, frustratingly so, and the share price is down 15% over the past 12 months. It is a bigger weight in the fund so has had more of an impact.

We got excited in 2018 when the new chief executive came in and promised to reposition the company by selling off a lot of the low-growing operations and re-investing in exciting areas.

Over the past few quarters, it has missed market estimates and has been losing market share. Last week the chief executive left and the company has brought in a Nestlé lifer. I think it is a really interesting investment now. It probably has another couple of tough quarters until it can reset but, over the long term, I think the investment case is going to reinvigorate itself. I would be a strong buyer at this price.

Is there a stock you wish you could buy?

Costco, which now yields 0.5%. The business model is phenomenal and the share price is up 60% in the past 12 months. I am kicking myself because we looked at it and did buy it for some of the growth funds but not the income fund.

With its membership model and management team, Costco is a sublime operation and it is my favourite shop – I love going to the one in Edinburgh. I’ve always wanted to be a shareholder but trading on a price-to-earnings ratio of over 50x and paying a yield of 0.5% – we’d be pushing the boat out too far to justify owning it in the portfolio.

What do you do outside fund management?

I am an avid walker. I spend a lot of time climbing hills and love doing Scotland’s longest walks like the West Highland Way. I have walked from Glasgow to Inverness. I am also a ridiculously keen armchair sports fan.