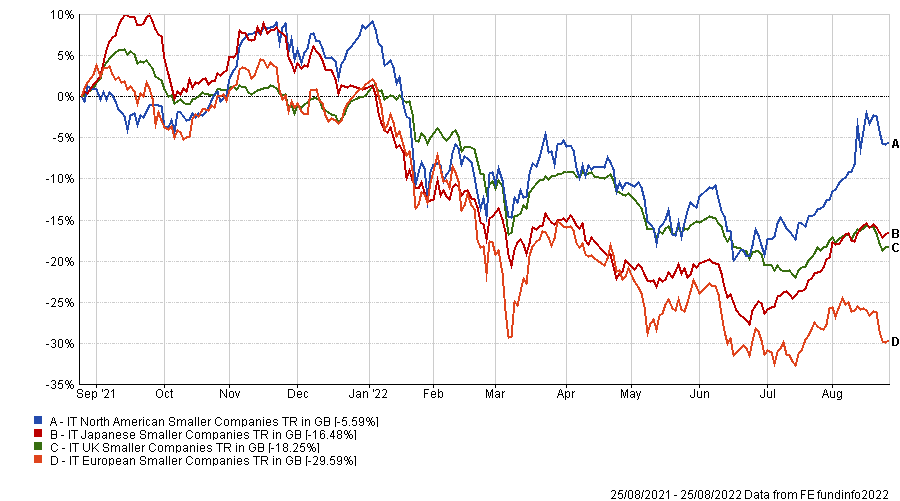

Smaller companies have suffered in the UK and Europe this year, but outside these regions, they are holding up surprisingly well, according to Peter Ewins, manager of Columbia Threadneedle’s Global Smaller Companies Trust.

“I think Europe and the UK are much more in the maelstrom of the European gas problem, the Russian conflict and the inflationary crisis,” he said.

“US small caps are actually not doing too badly this year, and neither are Japanese ones.”

Performance of the AIC small cap sectors over 1yr

Source: FE Analytics

However, he said this doesn’t mean investors can become complacent in this area of the market, as there are still plenty of companies that can lose everything.

In the interview below, the manager reveals where he sees opportunities, what sectors he has been buying more of and which ones he’s been avoiding.

Can you summarise your process in three sentences?

We aim to deliver to investors a broad exposure to smaller companies around the world.

We look at the smaller companies universe through a fundamental and layered approach, trying to identify high-quality businesses with good management teams that will deliver growth. We buy them at sensible valuations and back them over the medium term.

Investing in smaller companies is more about growth than income from our perspective, but this structure has delivered both over time.

What have been your best calls of the past year?

Where we have done best over the past year has come down to takeovers.

In the year to April, 12 out of 17 takeovers were UK names, including the recent RPS Group, Euromoney, Telecom Plus – which recently benefited from consumers trying to save costs on their utility bills – and insolvency services business Begbies Traynor. Brewin Dolphin was also taken over on a very large premium.

In the US, we have a few plays on the agricultural scene, with American Vanguard and The Andersons, which, a bit sadly, profited from the high price of agricultural products brought about by the Ukraine war.

We also expect the recent purchase of Kosmos Energy, which has assets in the US and offshore Africa, to benefit from the rising production of liquified natural gas, helped by the outlook for higher prices.

What holdings have disappointed?

In the UK consumer area, Treatt and Hotel Chocolat have both downgraded expectations of late.

In the US, Hayward Holdings, a swimming pool equipment business, has seen a destocking phase which led to a recent downgrade. This has also affected the share price of Fluidra, another swimming pools holding we have in Europe.

How has your portfolio changed lately?

On the consumer side, we have sold down some names where the cost-of-living crisis will be a major problem.

We have been adding to energy services – including equipment rental for oil & gas and renewables markets.

In Europe, we added the Bank of Ireland, which we expect to do well, helped by the rising interest rate environment.

More defensive plays in the UK have been the hospitality and annuities sectors, and we also tried to capture value in areas which had got too expensive, but which have now pulled back, like real estate.

Are there any sectors that you won’t invest in?

There's quite a lot of companies listed in North America that are involved in biotechnology, working on drugs that are going through trials. If the trials are successful, they can multiply your money, but if they're not, you can virtually lose everything.

We are also cautious about loss-making companies that have no history of profitability. That's not to say we won't occasionally invest in a loss-making business, but they will tend to be companies that are going through a rough patch but for which we can see a recovery coming through.

Nor do we make a lot of start-up investments. We won’t buy, say, an e-commerce platform that seems set to do great things but ultimately has no history of actually delivering returns.

We generally avoid speculative investments as a whole and risky investments such as mining, where it’s all about large caps.

What are your top three holdings and how likely are they to change?

They are three collective investments in Japanese equities. Before BMO was acquired by Columbia Threadneedle, we felt that it would be better to use collectives for that part of the world. There wasn't a huge dedicated smaller companies investment team for Japanese small caps, and that was a good opportunity to really look in detail at company fundamentals.

But as we're part of a bigger group now, the situation could evolve.

How do you incorporate environmental, social and governance (ESG) factors?

We have always looked at ESG factors before making an investment.

Global governance has always been a major issue in small caps, where investors want to be confident that the board structure is sensible.

In terms of the ‘social’ element, we’ve stepped up our evaluation of companies, and we have considered whether to attach a premium or a discount for any ESG issue within a valuation.

But ultimately, we spend a lot of time doing what we've always done, which is focusing on the fundamentals of the business case, and there will be varying importance to ESG factors within any individual company and within different sectors.

How do you use gearing?

The board's view has been that the trust should be geared at most points. Their view is that over time, financial markets go up, and you want to be able to enhance returns.

A consistent approach to gearing gives you benefits when markets go up, while the opposite approach of being more tactical is quite difficult to get right.

We keep a fairly consistent level of gearing, no higher than 4 or 5%, because smaller companies can be quite volatile.

What do you do outside of work?

Sport is my main thing: football, tennis, golf. Then being a father – I also provide a taxi service to my kids, driving them to their sport practice. Then travelling. It’s a busy old life, really.

Performance of trust vs sector over 1yr

-5.png)

Source: FE Analytics