UK gilt yields climbed to their highest level in decades earlier this year, offering investors a yield of more than 4% but veteran bond manager Richard Hodges cannot see a good reason to invest.

The FE fundinfo Alpha Manager argued that gilts and sterling corporate debt offer little real value to investors. Instead, he has found the most attractive government bonds in regions outside the UK.

For example, he pointed to Romanian and South African sovereign debt, which offered yields of around 6.3% and 11% at the time of writing, well above what you could get in the UK. “Imagine the level of volatility you can realise but still achieve a positive return”, he explained.

It led the manager of the Nomura Global Dynamic to proclaim that he would invest in “government bonds over investment grade credit all day, every day”.

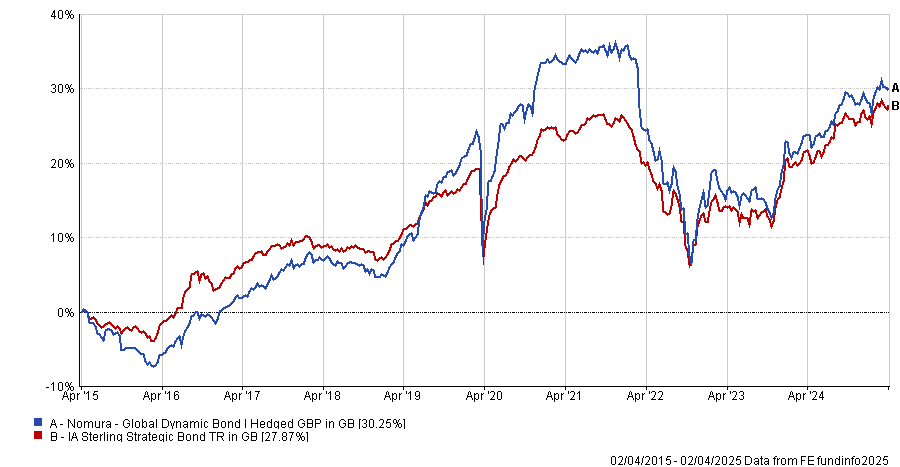

Performance of fund vs sector over the past 10yrs

Source: FE Analytics

Below, he also talks to Trustnet about why Russia was one of the worst calls he made in years, why flexibility is so important to the fund, and why large allocations towards high yield bonds are inappropriate in today’s market.

What is the fund’s process?

We identify and purchase bonds that will deliver attractive total returns in the prevailing environment. We like to describe our approach as ‘unconstrained’, but its more accurate to say we are highly flexible with very few constraints in terms of geographical reach or credit rating.

We use simple hedging techniques to control the exposures to credit risk and duration, aiming to reduce volatility through periods of market stress.

What differentiates your fund from its peers?

When we describe ourselves as ‘flexible’ we really mean it and we try to actively move the fund to benefit from the changing environment.

Sometimes we make changes slowly, but when unusual opportunities present themselves (for example at the start of the pandemic), we will move quickly to try and capture them.

From time to time, we will actively hedge the fund through periods of volatility. While other fixed income funds have access to the same hedging tools as us, we rarely hear competitors use them in the same way.

You have a very low allocation towards high yield. Is this a structural or tactical decision?

High yield bonds currently have very tight spreads, despite an increasing need for high yield firms to refinance that debt in the years ahead. We find better opportunities elsewhere, such as emerging markets or in the subordinated debt of European banks.

In the past, we have had allocations to high yield of more than 30% (at the risk of being a broken record: when we say we are flexible, we mean it) but it is not appropriate for the current fixed income market.

Duration is around five years – is this about average?

It is but it has changed significantly and we have had duration as high as eight years before. For example, after the Brexit vote in 2016, the protective hedges we had in place to guard against volatility included US treasury options that went rapidly into-the-money pushing duration to 10 years intraday.

By contrast, back in 2021, when major central banks told us that inflation was ‘transitory’, we thought differently, and built a short position in two-year and five-year US treasuries that pushed our Fund duration as low as two years.

2017-2021 were very strong years for the fund. What worked so well?

It was a wide range of environments, with a wide range of drivers for the fund. In 2018, the Fed hiked rates, which caused a poor environment for all fixed income markets, which is where our hedging came to the fore.

By contrast in 2019, risk assets were very strong and positions in European sovereign bonds (Portugal and Italy) were our best performers.

In 2020, hedging was vital in smoothing volatility when risk assets plunged during the pandemic. We also pivoted into investment grade credit, which offered extraordinarily positive returns for the first time in the fund’s history.

As risk markets then recovered, we moved ahead of markets into higher yielding, riskier assets in both credit and emerging markets.

Why did the fund struggle more than its peers in 2022?

One word: Russia. We held 5% of the fund in Russian sovereign bonds, which yielded 9% and the country had a debt to GDP ratio of 19%, while every analyst was certain that no invasion of Ukraine was on the horizon.

We were wrong. Following the invasion, sanctions from the Russian bank forced us to mark the bonds to zero and we rapidly had to exit our roubles hedges, which were hedging an exposure we no longer had.

What do you do outside of fund management?

My golden retriever has an insatiable desire for walks, even when the weather is atrocious, and I spend most of my time satisfying that demand.