Donald Trump’s Liberation Day tariffs and his unconventional, unpredictable approach to policy-making is giving investors a headache. This year’s sell-off in US equities, especially the largest tech stocks, adds to the sense of foreboding.

As Darius McDermott, managing director of Chelsea Financial Services, said: “Donald Trump’s Liberation Day has markets on a knife-edge. Investors today must contend with what we like to call ‘TILT’, or Trump-induced liquidity turbulence – a world in which one tweet, one tariff, or one interest rate surprise can send markets reeling.”

For investors unsure of how to position their portfolios amidst the maelstrom, McDermott suggested a barbell approach. He highlighted a range of funds exposed to long-term trends and structural shifts, balanced out with bond funds to provide ballast.

“In a world where Trump-induced liquidity turbulence can turn markets upside down overnight, the winners will be those who look past the noise and focus on the bigger picture,” he stated.

One bigger picture trend is the revival of the European economy. Europe is stepping out of America’s shadow with commitments to increase infrastructure and defence spending through initiatives such as Germany's fiscal reforms and the European Union’s ReArm Europe programme.

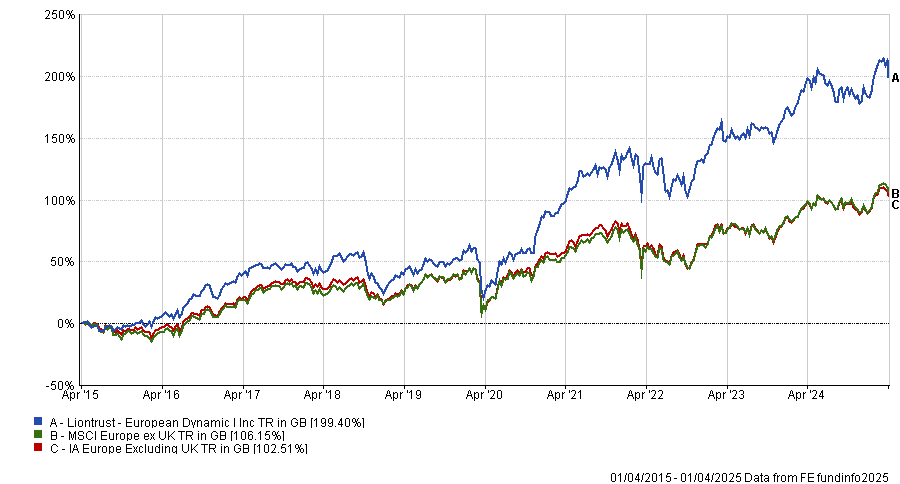

“In the European economy, innovation is booming,” McDermott said. One fund poised to ride the wave of Europe’s resurgence is Liontrust European Dynamic, which “zeroes in on resilient, high-growth businesses”.

The £1.8bn fund is managed by James Inglis-Jones and Samantha Gleave, who focus on historical cashflow performance and aim to buy companies that are generating a high cashflow for their asset base or market capitalisation. The investment process includes market regime indicators, which guide the fund managers’ market outlook and style tilts.

Liontrust European Dynamic is the second-best performing fund in the IA Europe Excluding UK sector over 10 years to 1 April 2025 and the third-best over five years. It has an FE fundinfo Crown Rating of five, placing it within the top 10% of its sector for alpha generation, controlled volatility and consistent outperformance over the past three years.

Performance of fund vs sector and benchmark over 10yrs

Source: FE Analytics

Closer to home, the UK’s small and mid-cap companies offer “a hotbed of underappreciated potential”, McDermott said. “With strong balance sheets and serious growth prospects, these companies are well-placed to thrive over a longer horizon.”

Strategies unearthing these hidden gems include Rosemary Banyard’s VT Downing Unique Opportunities fund and Rory Bateman’s Schroder British Opportunities investment trust, he said.

Banyard joined Downing in March 2020 to launch the Unique Opportunities fund, having previously managed money at Sanford DeLand and Schroders, where she ran the Schroder UK Mid Cap fund, amongst other strategies.

At Downing, she oversees a portfolio of 25-40 stocks that she believes have a unique outlook and enduring competitive advantages that are difficult to replicate.

At Schroder British Opportunities, Bateman and his colleagues invest in fast-growing young businesses across public and private equity markets. Unquoted holdings include: Easypark, which helps drives find and pay for parking; Expana, which provides global commodity price data; and Cera, a home care and healthcare company.

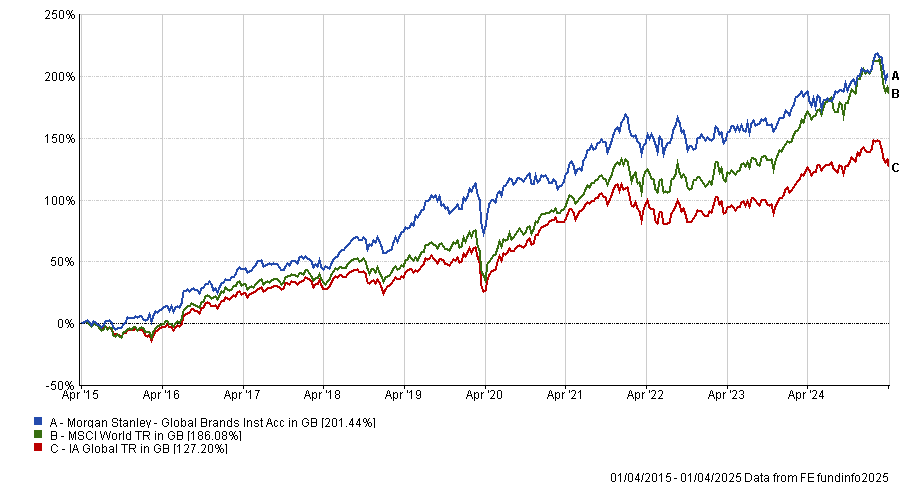

For investors who prefer a broad global mandate, McDermott highlighted Morgan Stanley Global Brands, which “provides exposure to world-class companies with serious pricing power – the kind of companies that weather storms and keep customers coming back, recession or not”.

William Lock, head of international equity, runs the fund with a large team. He and his colleagues look for high-quality companies with dominant market positions and powerful intangible assets.

Performance of fund vs sector and benchmark over 10yrs

Source: FE Analytics

For investors willing to cast the net a bit wider, McDermott proposed looking at infrastructure funds such as First Sentier Global Listed Infrastructure. Essential services such as transport, utilities and energy should continue to grow, regardless of who sits in the White House, he observed. American Electric Power Co. and National Grid are the £1.3bn fund’s largest holdings.

Performance of fund vs sector and benchmark over 10yrs

Source: FE Analytics

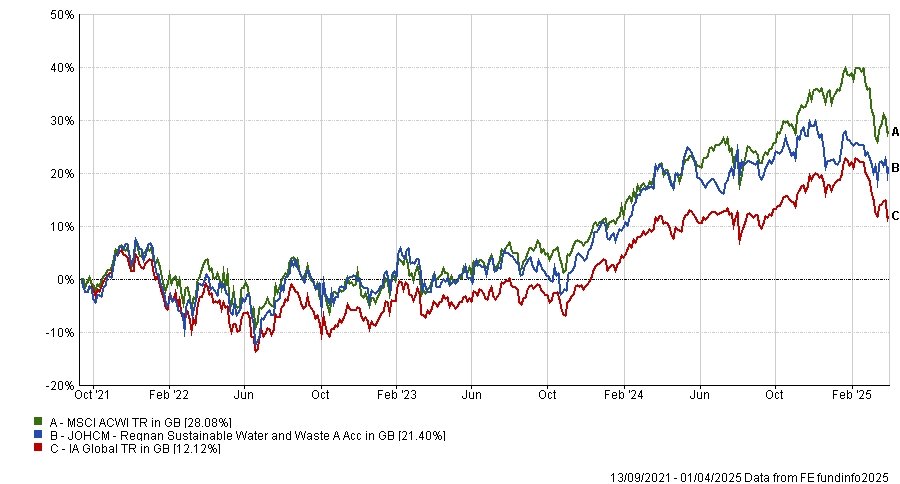

Sustainable investing is another long-term theme and here, McDermott’s pick was J O Hambro Capital Management’s Regnan Sustainable Water and Waste fund. “It focuses on companies tackling the global water crisis and waste management challenges, sectors that are only set to grow as populations rise and regulations tighten,” he said.

The fund was launched in September 2021 and is managed by Bertrand LeCourt and Saurabh Sharma.

Performance of fund vs sector and benchmark since inception

Source: FE Analytics

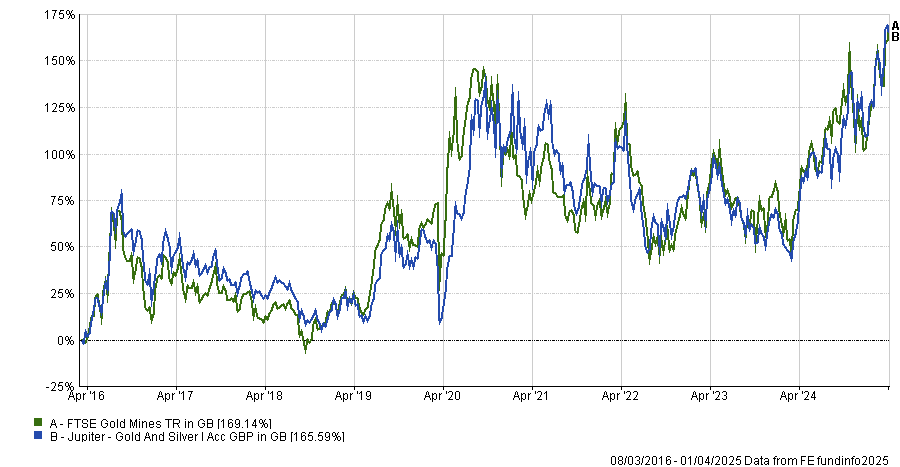

Another strategy providing an element of diversification is Ned Naylor-Leyland’s $1bn Jupiter Gold & Silver fund. “Tangible assets should provide a complementary hedge, particularly given central banks’ penchant for flip-flopping on rates and inflation refusing to stay buried,” McDermott said.

“Jupiter Gold & Silver offers exposure to precious metals and mining equities, ensuring a portfolio isn’t entirely at the mercy of central bank indecision.”

Performance of fund vs benchmark since inception

Source: FE Analytics; the fund has two benchmarks – the gold price and the FTSE Gold Mines index

Finally, McDermott suggested adding an anchor to the portfolio in the form of Invesco Bond Income Plus, an investment trust focusing on high-yield bonds. “With Trump the ringmaster of daily volatility, investors will need some ballast in their portfolios and bonds can do just that,” McDermott said. “Invesco Bond Income Plus delivers steady income streams while insulating against wild market swings.”

The trust had a dividend yield of 7.1% and was trading at a 1.7% premium as at 1 April 2025.

Its managers, Edward Craven and Rhys Davies, invest across three areas of the high-yield bond market: income generators (bonds issued by non-financial companies that pay a high level of income to compensate for their leveraged balance sheets); banks and subordinated financials (which are paying a premium over other areas of the market); and credit-intensive bonds (which have come under price pressure but which Craven and Davies believe have the right plans in place to turn things around).