Markets have been thrown into chaos after Donald Trump’s ‘Liberation Day’ caused global stocks to drop amid rising uncertainty and a deteriorating geopolitical picture.

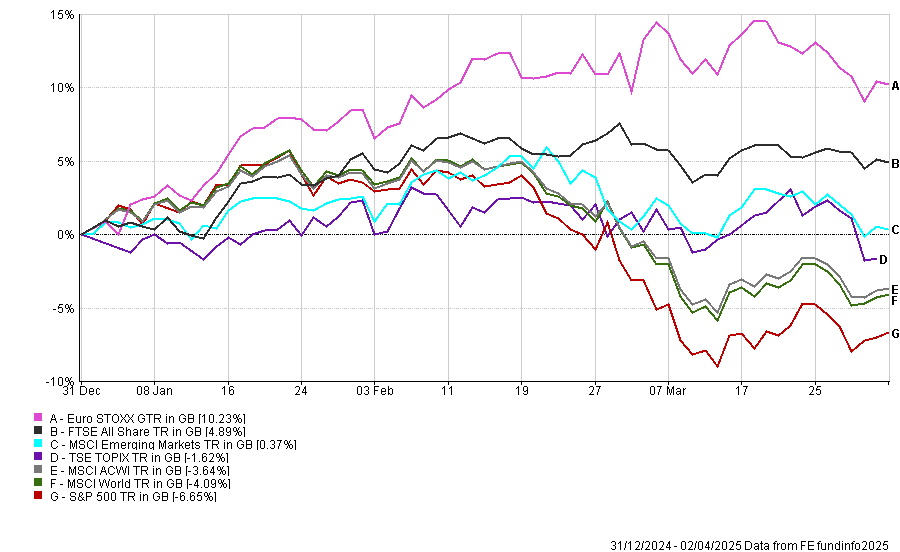

Investors may view now as a good time to diversify, particularly away from the US market, which has come under pressure already so far in 2025. Indeed, the S&P 500 is down 6.7% in sterling terms so far this year. Of the main market indices, only two – Europe and the UK – are in meaningfully positive territory, as the below chart shows.

Performance of indices in 2025 so far

Source: FE Analytics

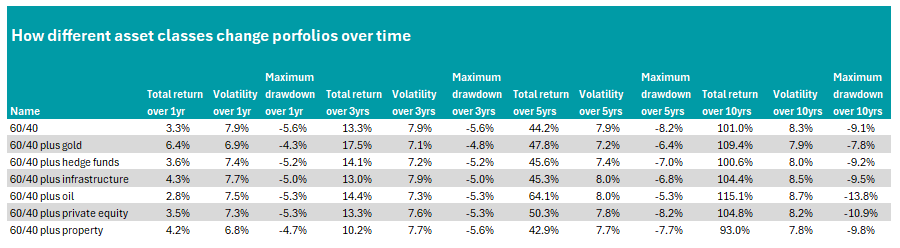

While one option may be to increase the allocations here, as some have suggested, there are alternatives to consider. As such, Trustnet has looked at how portfolios can be changed by adding a new asset to the mix.

To do this, we have taken a traditional 60/40 portfolio in equities and bonds, represented by the MSCI World and Bloomberg Global Aggregate index respectively, as a baseline for a balanced investor.

We then took a proportionate amount from each allocation and added a 10% weighting in different asset classes. For gold, we used the S&P GSCI Gold Spot index. We also looked at hedge funds (HFRI Fund Weighted Composite index), infrastructure (FTSE Developed Core Infrastructure index), oil (S&P GSCI Brent Crude Spot), private equity (IT Private Equity sector) and property (IT Property – UK Commercial sector).

We analysed each portfolio’s performance over one, three, five and 10 years, as well as the difference in the volatility and maximum drawdown (the amount an investor would have lost if buying and selling at the worst possible times).

Over the past 12 months, adding almost every alternative asset class would have benefited investors, except oil, which would have lowered returns. All the asset classes we looked at would have reduced the maximum drawdown and lowered the overall volatility of a portfolio, as the table below shows.

Source: FE Analytics

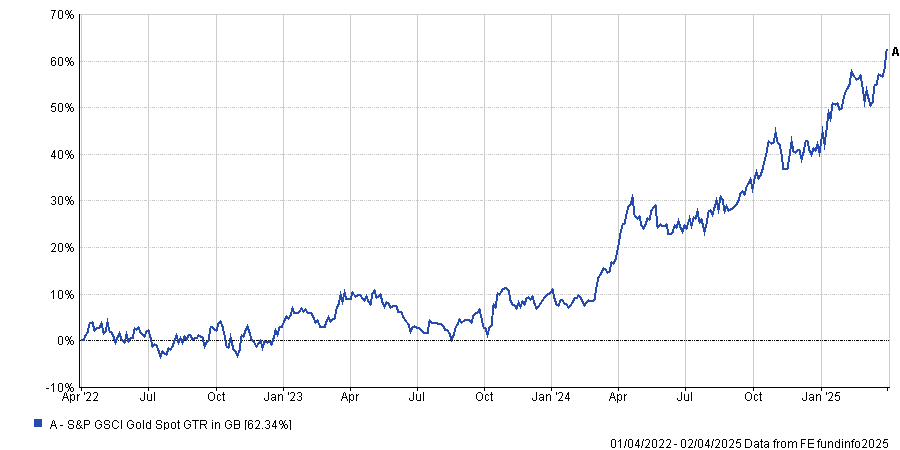

In the shorter timeframes (over one year and three years), the best addition to a portfolio would have been gold. Returns from a portfolio with 10% in gold were almost double that of a traditional 60/40 portfolio over 12 months, with investors making 6.4%, and were four percentage points ahead over three years.

The gold price has rocketed over the past few years as uncertainty surrounding the US government, war in Europe and the Middle East, and a generally fractured global landscape have caused investors to look towards safe havens.

Performance of index over 10yrs

Source: FE Analytics

This week, gold rose again after US president Donald Trump’s ‘Liberation Day’ in which he unveiled a bevy of new tariffs on countries around the world.

However, Adrian Ash, director of research at BullionVault, noted the rise was only in dollar terms as the currency sold off. The spot price fell in euro and sterling terms.

“Longer term, however, the reasons behind gold’s stellar start to 2025 are only stronger now that Trump has announced his tariffs. Weaker trade, higher input costs and shrinking margins are badly hurting the stock market, while geopolitical mistrust is deepening. Such a gloomy outlook for economic growth offers the perfect backdrop for further gains in gold,” he noted.

The precious metal has proven popular with investors, especially so far in 2025, when funds specialising in gold were among the most bought portfolios in the first quarter.

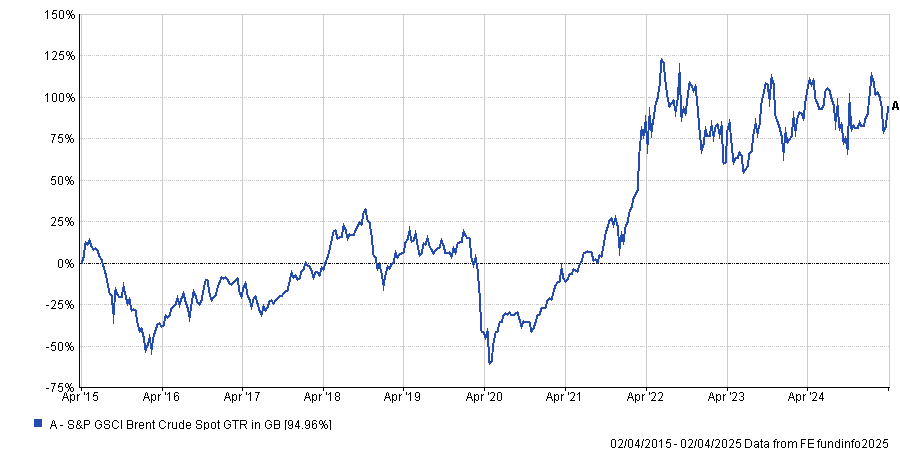

Over longer timeframes, oil has been the best place to put additional cash, with the spot price rising significantly since the Covid pandemic in 2020 and up some 95% over the past decade.

Performance of index over 10yrs

Source: FE Analytics

Last month, Nick Kirrage, manager of the Schroder Income fund, said oil will not stray too far from its current level from this point onwards but remains a compelling investment case nonetheless.

Adding 10% of a portfolio to an oil exchange-traded fund tracking the Brent crude spot price would have added around 14 percentage points over the past decade, with much of this coming in the past five years. However, it would also have increased maximum drawdowns and volatility as the asset class is not a traditional safe haven.

Next up was gold, which would have added around 8 percentage points over 10 years, while infrastructure and private equity also enhanced returns and lowered volatility (although the maximum drawdown was higher on both).

Only property and hedge funds failed to add meaningfully to a 60/40 portfolio over the long term, although the former has been a strong addition over the past year, while the latter has served investors well in the medium term.