The UK stock market’s resurgence this year, followed by early August’s rapid fall and subsequent rebound, have brought to bear the importance of both downside protection and upside capture.

To give investors a smoother ride and get the best of both worlds, fund selectors often pair defensive strategies with complementary funds that seek to maximise gains during market rallies.

To that end, Trustnet asked fund selectors to pair up a cautious UK equity strategy with a fund or trust poised to thrive in rising markets. These UK fund picks follow recent bull/bear pairings in Asian and global equities.

Mercantile and City of London

Columbia Threadneedle Investments’ Peter Hewitt, who runs the CT Global Managed Portfolio trust, paired City of London with the Mercantile investment trust. The former is an equity income trust with a large-cap bias while the latter focuses on mid-cap growth companies.

“There’ll be virtually no overlap in the portfolios,” Hewitt said. “The difference between City of London and Mercantile really is north and south pole.

“City of London will give you some capital upside but in a strongly moving up market, it probably will lag a bit. In a falling market, unless the fall was very definitely concentrated on the FTSE 100, it would tend to fall by a bit less.”

By contrast, Mercantile “really does move sharply on the upside when markets are pushing on and they’re being led by mid- and small-caps,” he said, for instance in December 2023 and June and July 2024.

UK mid-caps have rallied in fits and starts during the past six-to-eight months but Hewitt hopes they will perform more consistently for the rest of this year and into the next.

Performance of trusts vs FTSE All Share over 10yrs

Source: FE Analytics

Mercantile is run by FE fundinfo Alpha Manager Guy Anderson, who Hewitt described as a good stockpicker, and his colleague Anthony Lynch at JPMorgan Asset Management.

The trust is trading on a 9.1% discount (as of 26 August) and has a 2.9% prospective dividend yield.

City of London, meanwhile, has a 4.7% yield (as of 23 August 2024) and has grown its dividend for 58 consecutive years – the longest track record amongst the Association of Investment Companies’ ‘dividend heroes’.

It holds 70-80% of its portfolio in FTSE 100 names, investing in dividend-payers such as Shell, BP, banks and insurance companies.

“The discount/premium is managed quite well, it never goes to much of a discount or premium,” Hewitt noted, as the trust has “consistently issued shares”.

He described the trust’s manager, Job Curtis from Janus Henderson Investors, as “very solid, cautious, conservative – all that you’d want from a UK income manager”.

Liontrust UK Growth with Schroder Recovery

Nick Wood, head of fund research at Quilter Cheviot, suggested pairing Liontrust UK Growth with Schroder Recovery.

The former is run by Liontrust’s Economic Advantage team with an emphasis on large-cap stocks. At least 90% of the portfolio is held in FTSE 350 companies and its top 10 holdings include BAE Systems, Shell, BP and Hargreaves Lansdown.

Wood said: “The process is focused on higher quality companies with some sort of durable competitive advantage, which allows them to earn above-average profits. This results in a portfolio that tends to perform well in difficult markets, whilst the superior stock selection over time has resulted in very strong long-term performance.”

Performance of trusts vs FTSE All Share over 10yrs

Source: FE Analytics

Schroder Recovery has “a much more volatile profile”, but “has demonstrated strong stock selection over time”, Wood continued.

It is managed by the value team at Schroders, led by Nick Kirrage, which has “consistently outperformed expectations, beating the market over the longer term even when its style is out of favour”.

With UK equities remaining relatively unloved – although outflows have slowed – Wood thinks this fund could benefit from a double discount by selecting the cheapest companies in an undervalued region.

The fund selects stocks that have suffered short-term setbacks and, due to its contrarian nature, performance can diverge significantly from its FTSE All Share benchmark. Nonetheless, “over the long-term this should mean plenty of opportunities for above-average returns”, Wood observed.

The fund currently has a bias towards small- and mid-caps, which boosted performance during the recent rally, spurred by interest rate cuts.

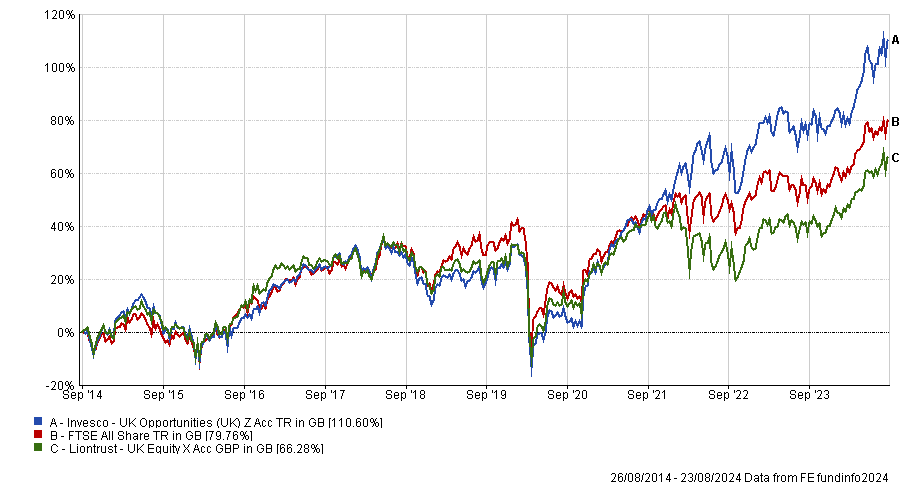

Invesco UK Opportunities Fund alongside Liontrust UK Equity

John Husselbee, head of Liontrust Asset Management’s multi-asset team, holds Invesco UK Opportunities alongside an in-house fund, Liontrust UK Equity.

Performance of trusts vs FTSE All Share over 10yrs

Source: FE Analytics

Invesco UK Opportunities, managed by the “highly experienced” Martin Walker, is a concentrated best ideas fund which typically holds about 40 names. It has a bias to large-cap value stocks, many of which are global leaders in their industry.

“We will typically blend more than two funds in our investment process but Liontrust UK Equity would perhaps be the most appropriate to construct a complementary pairing,” Husselbee said.

Imran Sattar became sole manager of Liontrust UK Equity in November 2023 due to James De Uphaugh’s retirement. He has reshaped the portfolio, shifting the focus towards quality growth, according to Husselbee. Sattar pursues a high conviction approach, investing in advantaged businesses that can perform over the economic cycle.

“A high active share is a factor we consider, as we are always conscious in blending managers we don’t just recreate an expensive index tracker,” Husselbee added.