Many companies reported second quarter earnings in July. Although the results have been mixed, so far we have seen fewer positive surprises than in any quarter since the height of the COVID-19 pandemic.

In an environment of political uncertainty and signs of macroeconomic weakness, it is timely to again consider one of the key questions for investors: are they being paid to take risk within credit?

This is not a question of whether spreads are attractive at current levels, but whether within corporate credit specifically – European investment grade – investors are being adequately compensated to take additional risk of varying forms.

This has been a frequent topic of conversation with clients throughout 2024. In response, we have that argued investors now need to be more discerning about where they take risk relative to the past two years and that fundamental research will become even more important.

The spread rally seen since the middle of 2022 has compressed many traditional sources of additional credit spread. Whilst we do not believe there is a need to immediately reduce risk in our portfolios, we do believe an ‘up-in-quality’ bias makes sense over the coming months.

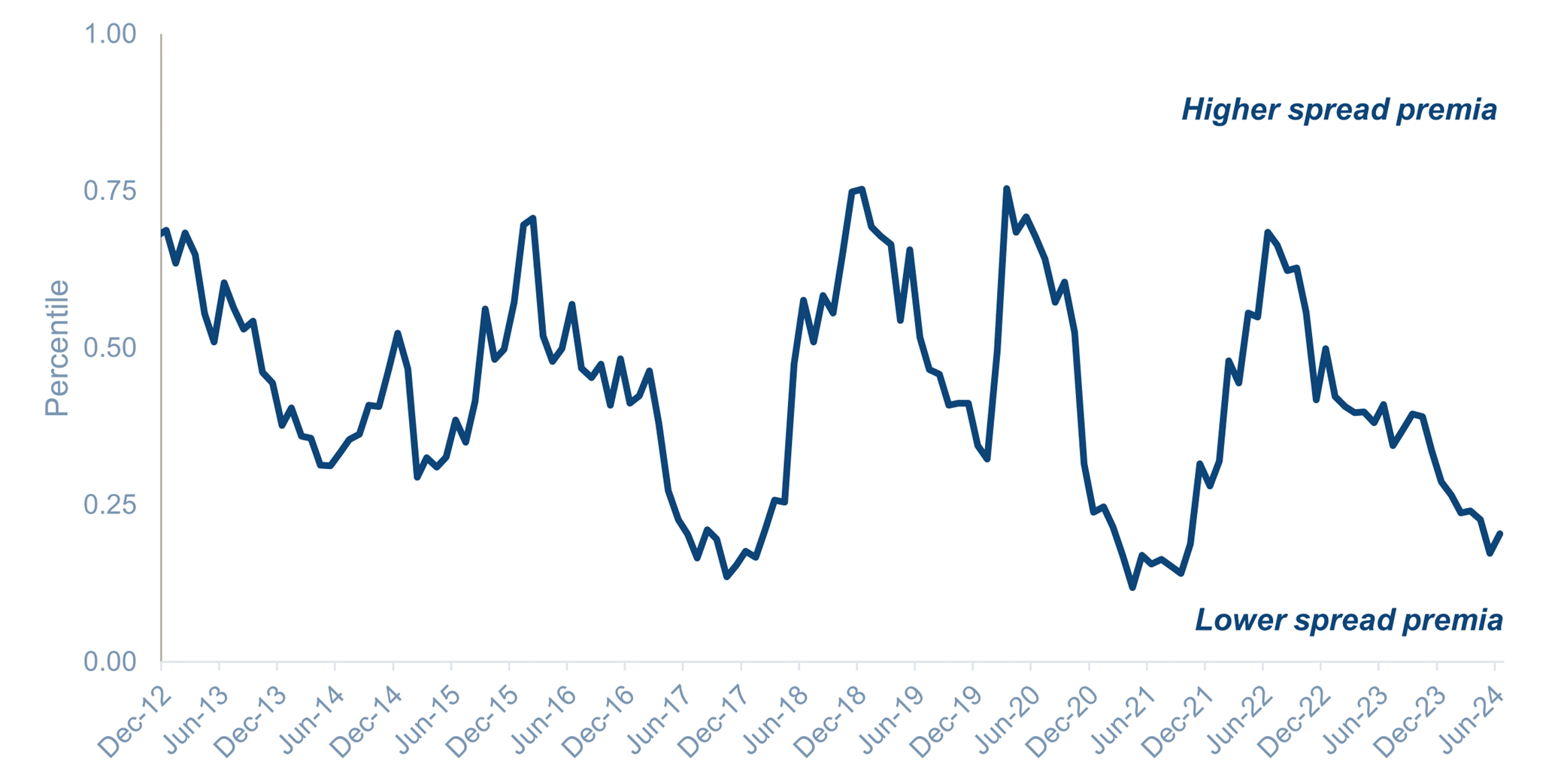

Quantifying spread premia

To quantify where spread premia are versus historic levels, we have constructed an internal reference index for European investment grade using five simple inputs: ratings, sector, subordination, curve (the spread difference between longer-dated and shorter-dated bonds) and peripheral versus core (the spread difference between instruments from peripheral and core European issuers, in recognition of perceived geographic risk).

Based on our opinion and analysis, we have focused on traditional sources of risk in the market. We believe these five factors (credit risk, subordination risk, interest rate risk, geographic risk and sector risk) are the key risks for which investors would typically expect a spread premium.

A spread premia index for European investment grade

Sources: ICE BofA Platform and Muzinich, monthly data as of 30 Jun 2024; the spread premia indicator calculated here is based on the spread-to-worst versus government bonds provided by the ICE BofA Platform

As shown, spread premia are close to their historic lows, although not in uncharted territory. Reaching these levels of spread premia has not historically prompted a sudden reversal and a decompression of spreads. We can – as seen in 2017 and 2021 – remain at these compressed levels for some time.

It is also possible for credit spreads at a broader level to continue to tighten. However, the potential additional return from spread tightening in higher beta parts of the market would appear to be limited if history is any guide.

Ian Horn is a portfolio manager at Muzinich & Co. The views expressed above should not be taken as investment advice.