The deadline for investing your £20,000 ISA allowance is on Saturday 5 April but with Donald Trump poised to unveil his ‘Liberation Day’ tariffs this afternoon, investors may be understandably reluctant to put new money into the stock market this week, given there is so much uncertainty over how markets will react.

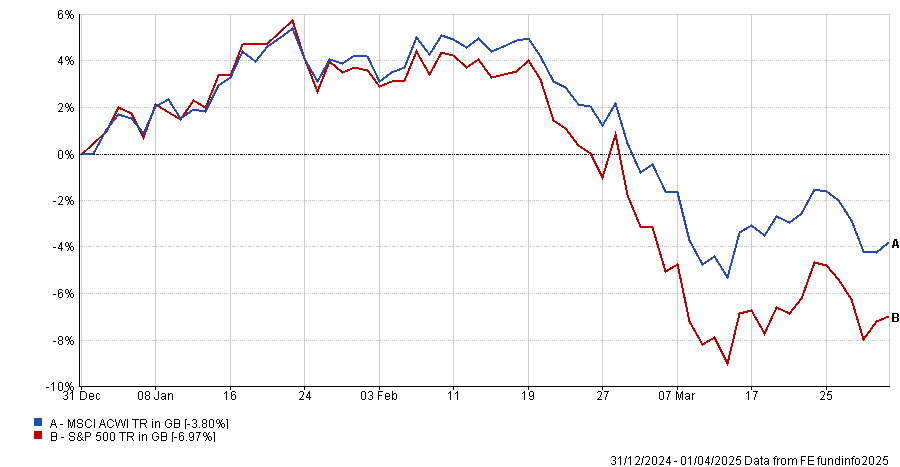

Another factor making some investors nervous is the sell-off in US and global equities. Between 19 February and 1 April, the S&P 500 has lost 10.6% in sterling terms and the MSCI All Country World Index (66% of which is in the US) is down 8.4%.

Performance of US and global equities year-to-date

Source: FE Analytics

That being said, the ISA allowance refreshes every tax year so investors who can afford to commit the full £20,000 need to do so this week or they will lose this year’s allowance.

Investors can split the allowance between a cash ISA and a stocks and shares ISA however they see fit.

Given the current stock market turbulence, keeping money in cash may seem appealing. Cash ISAs are delivering fairly attractive returns currently, with several providers offering rates of 4.4% or higher, according to MoneySuperMarket.

Over the long-term however, investing in equities or in a multi-asset portfolio has the potential to significantly outperform cash, according to Vanguard’s data.

Investing £20,000 in a stocks and shares ISA today with a long-term expected return of 6% would result in a pot of around £64,000 in 20 years’ time. By contrast, a 2.5% expected annual rate of return from cash over 20 years would turn £20,000 into £33,000 – almost half the amount of the stocks and shares ISA.

James Norton, head of retirement and investments at Vanguard Europe, said: “The difference of £31,000 is a year and a half’s worth of ISA contributions for someone maximising their allowance each year, demonstrating the reward for taking some investment risk, even amid uncertainty about short-term market conditions.”

Yet for people who want the chance to outperform cash but are reluctant to invest, there is another option that may serve as a halfway house.

“If you’re feeling particularly concerned about investing in the current market environment, there are still ways to make the most of your ISA allowance without taking on too much risk,” Norton said.

“One option is to temporarily park any remaining ISA allowance in a money market fund, which is a low-risk investment that gives you a place to hold rather than grow your savings, while aiming to give investors a slightly higher return than cash.

“Once you feel more confident, you could then consider moving your money into more growth-oriented investments that help you progress towards long-term goals.”

Money market funds come in different flavours. Those in the IA Short Term Money Market sector are lower risk and deliver returns similar to the Bank of England base rate, whereas those in the IA Standard Money Market sector have more flexibility and aim to achieve slightly higher yields, as Trustnet’s guide to money market funds explains.

For investors seeking a fund led by an experienced manager with a proven track record, three money market funds are run by FE fundinfo Alpha Managers: Craig Inches’ £7.5bn Royal London Short Term Money Market fund; Steve Matthews’ £1.1bn WS Canlife Sterling Liquidity fund; and Lloyd Harris’ £326m Premier Miton UK Money Market fund.

Darius McDermott, managing director of Chelsea Financial Services, sympathises with savers who are reluctant to invest in the current climate but, like Norton, he does not recommend sitting on the sidelines.

“Donald Trump’s Liberation Day has markets on a knife-edge. Investors today must contend with what we like to call ‘TILT’, or Trump-induced liquidity turbulence – a world in which one tweet, one tariff, or one interest rate surprise can send markets reeling,” McDermott said.

“With inflation still lurking in the background and interest rates and geopolitical uncertainty keeping everyone on their toes, we think investors need to engage with their portfolios a little more to make sure they are not caught out.”

McDermott suggested a barbell approach focusing on long-term, thematic investing, combined with safe haven assets such as bonds, as a way to capture the upside without suffering too much of the downside.

“Thematic investing essentially means aligning capital with long-term structural shifts and ignoring the short-term macro noise – it also means going against the grain until the herd (eventually) catches up. From British small-caps and global infrastructure to sustainability and hard assets, we think it is time to get ahead of the trends shaping tomorrow’s markets,” he said.

“This isn’t the time to sit on the sidelines. Thematic investing isn’t about chasing fads or timing the market – it’s about positioning capital in the right sectors before everyone else catches on. In a world where Trump-induced liquidity turbulence can turn markets upside down overnight, the winners will be those who look past the noise and focus on the bigger picture. And don’t forget to add protection.”