The Bank of England last week held off on another rate hike, leading some to consider how to shift portfolios to thrive in a peak interest rate environment.

Although rates could go a little higher over the coming months, Bank governor Andrew Bailey recently indicated that interest rates could be reaching their peak as inflation in the UK starts to come down.

The Bank carried out 14 rate hikes in a row, taking the base rate from close to zero to its current 5.25%. This caused significant market volatility but there could be another change in market dynamics when rates peak.

Rob Burgeman, investment manager at RBC Brewin Dolphin, said: “Markets don’t deal with today – they are more of a reflection of where we will likely be tomorrow. The share prices of property and infrastructure companies and trusts, for example, are currently going through a tough time because interest rates look likely to stay higher for longer. An investor buying into them will only do so for a yield that is over and above the risk-free return available on cash – up to around 5%.

“However, it seems likely that in two years’ time rates will be lower than they currently are. The companies that benefit from this reversal of interest rates are probably going to be some of the same ones which struggled as rates rose.”

Below, Burgeman highlights three parts of the market that have suffered while interest rates have been rising but might be in for better times when central banks stop hiking.

The first area that could benefit from peaking interest rates, he suggested, is commercial property: “Property has an innate gearing factor when it comes to interest rates – the value of property is a function of the risk and volatility of the rent coming in.

“You generally find that industrial property is highest yielding – manufacturers and other industrial occupiers tend to be economically sensitive – followed by distribution and then secondary offices.”

Commercial property has underperformed for some time because of rising interest rates and the after-effects of the Covid pandemic, which left more people working from home. Meanwhile, the cost-of-living crisis slowed spending in retail and leisure.

Because of this, the average trust in the Association of Investment Companies’ commercial property sector is trading on an average discount to net asset value of 26.7%. However, Burgeman added that there are some “perfectly good companies” that invest in commercial property.

Performance of trust vs sectors over 3yrs

Source: FE Analytics

He pointed to Primary Health Properties, an investment trust that owns healthcare facilities, such as GP surgeries. The trust resides in the IT Unclassified sector, but we’ve included the IT Property UK Commercial sector in the above chart for comparison purposes.

Burgeman likes the trust because its yield has climbed from around 4% to almost 7% over the past two years. This is down to the fact that the trust has fallen harder than its average peer, although it is well-regarded by analysts thanks to a strong history of dividend growth and high demand for its properties.

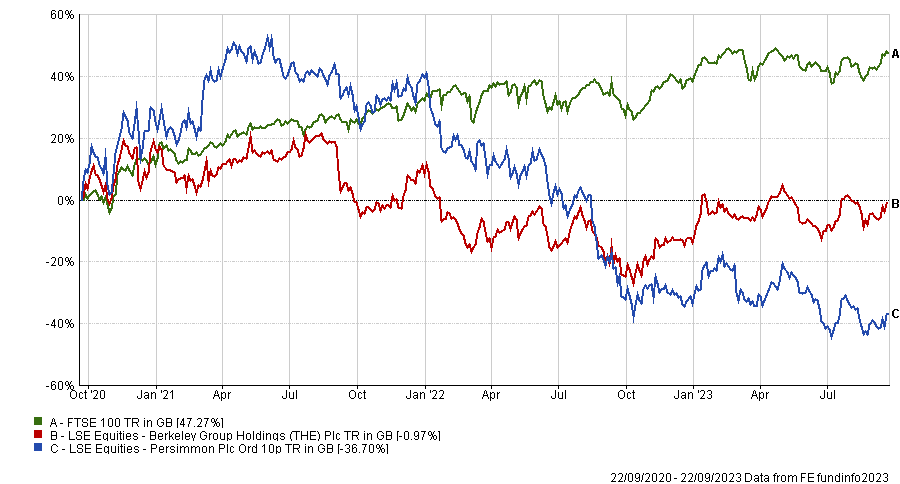

Housebuilders are another area that the RBC Brewin Dolphin investment manager expects to be attractive in a peak interest rate environment.

This is another part of the market that faced a tough time when rates were rising. The average two-year fixed rate on a 95% mortgage has climbed to nearly 7%, which makes it harder for people to buy a new home. As a result, house prices have fallen for several months and some of the UK’s housebuilders have reported slowing sales.

“The last time we went through a period like this in 2008 and 2009, housebuilders were on the edge of collapse,” Burgeman said. “But, this time round, they are in a much better position, with much stronger balance sheets. There are undoubtedly challenges ahead and they may well build fewer homes, but this is not the existential crisis that befell them 15 years ago.”

Performance of stocks vs sectors over 3yrs

Source: FE Analytics

He picked out two stocks in this area: Persimmon and Berkeley Group, both of which are members of the FTSE 100.

Burgeman said Persimmon “has long been seen as the blue-chip choice in the sector”. Slowing sales means it has had to cut its dividend hard, but the stock still yields more than 5% and trades on a relatively attractive forecast price-to-earnings ratio of just 13.8 times.

Meanwhile, he sees Berkeley Group as another quality name. It has more of a focus on mixed-use developments and while the stock has never been a great yielder it still offers over 2% and trades on a forecast price-to-earnings of 12 times.

The final area of interest when interest rates peak is retail. The ongoing cost-of-living crisis has left people with less disposable income and consumer confidence has weakened; because of this, the share prices of retailers have fallen.

“Retail – excluding supermarkets – has been a tough place to be for a while,” Burgeman said. “Not only did they have the Covid-19 enforced lockdowns between 2020 and 2022, but they have emerged into a cost-of-living crisis that has seen many people prioritise the necessities of life and, where they can afford to do so, holidays abroad to make up for the experiences lost during the pandemic.”

Performance of stocks over 3yrs

Source: FE Analytics

However, he argued that “there have been some bright spots in the sector defying the gloom”.

He highlighted FTSE 100 stock Next as one company that is bucking the trend in retail. It recently reported a boost in sales from the warm weather in late May and June, helping to lift its profit guidance for the full year for the third time.

Burgeman also likes Marks & Spencer, which has been restricting its business and shifting more towards online. This change in strategy is starting to pay off, which should help the company when consumers are no longer feeling as squeezed.